that have grown at a CAGR (compounded annual growth rate) of 47.5 percent in the past seven years")

Highlights

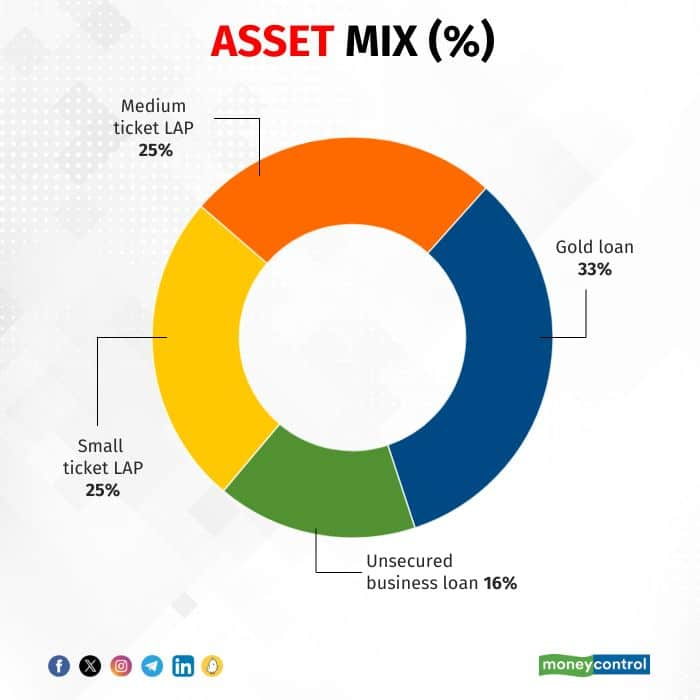

Fedfina is present broadly in four product categories and has a dominance of secured loans (close to 84 percent).

Source: Company

Investment Rationale

Robust growth to continue

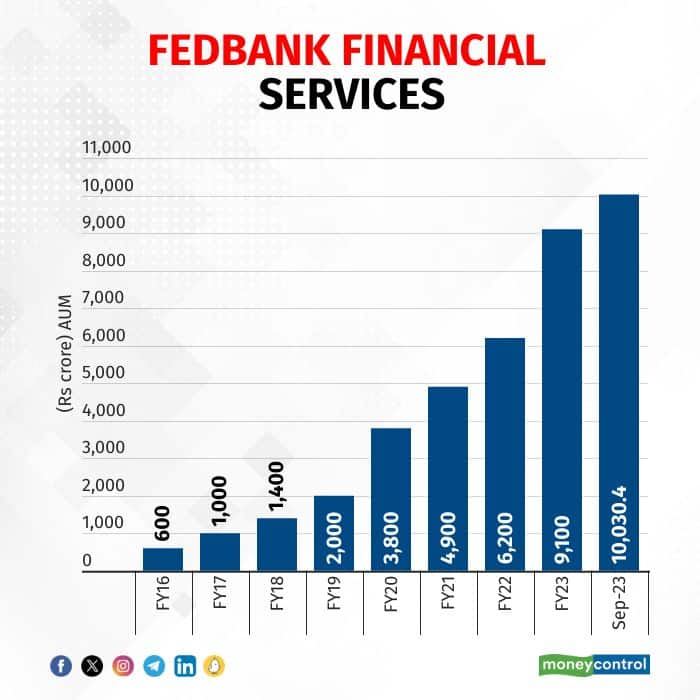

Fedfina has seen a strong traction in its assets under management (AUM) that have grown at a CAGR (compounded annual growth rate) of 47.5 percent in the past seven years — FY16 to FY23. At the end of the first half of FY24, the AUM crossed Rs 10,000 crore, showing a YoY growth of 38 percent.

Source: Company

The small size of the loan book — barely 30 basis points of the NBFC’s total advances — leaves ample scope for growth despite the heightened competition from banks and other NBFCs.

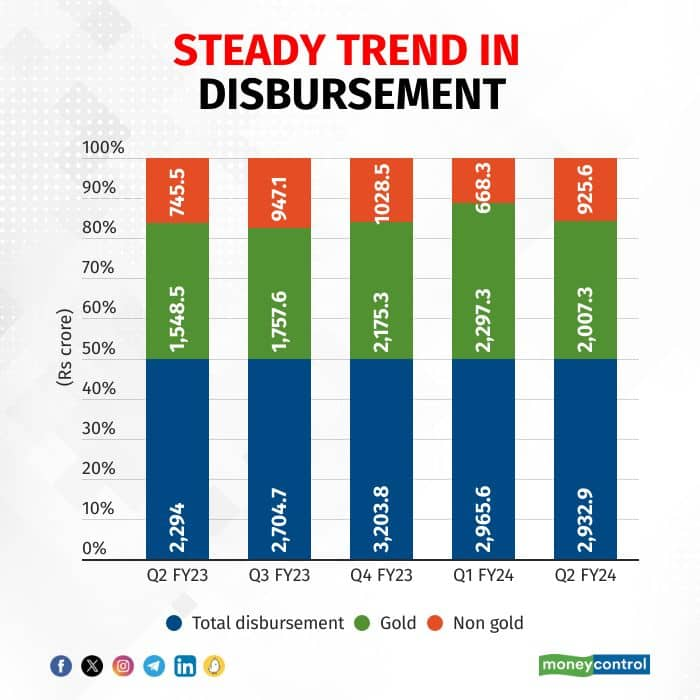

Disbursement too has been strong for both gold and non-gold loans.

Source: Company

Gold loan an attractive product

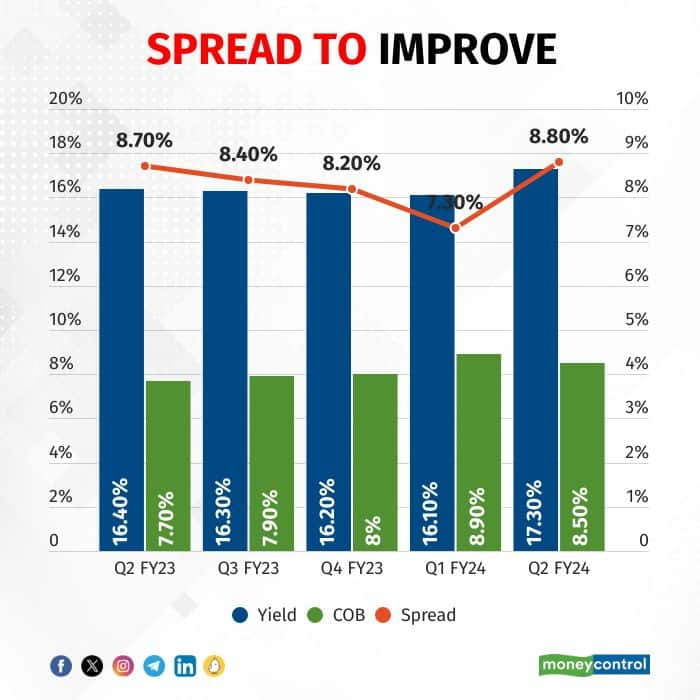

Fedfina has a strong presence in the gold loan business, which gives it a decent yield of close to 17.5 percent, much higher than what is charged by banks. To expand this business, the company has started co-lending tie-ups. Usually, the firmness in gold prices aids this business as customers can borrow more for the same quantum of gold pledged.

Source: Investing.com

Source: Investing.com

We, therefore, expect to see a strong traction in gold loans as well as non-gold where the higher level of economic activity in the second half of the year should help.

Spread expected to improve

Thanks to the improving lending yield, Fedfina has managed to improve the interest spread despite the firming up of the borrowing cost. However, recent RBI guidelines on increasing the risk weight on lending to NBFCs could increase borrowing costs, given its large (close to 76 percent) reliance on bank funding. The liquidity infusion through the IPO (around Rs 600 crore) should act as a cushion and help margin gains in the second half.

Source: Company

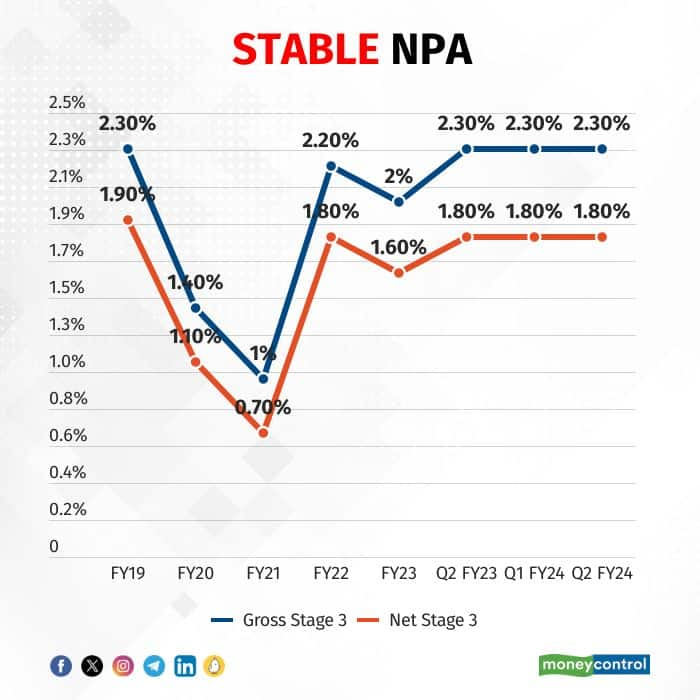

Asset quality – not much of a worry

With a largely secured book, there was no spike in asset quality that was seen in many unsecured-focused NBFCs during Covid. Gross and Net Stage 3 assets at 2.3 percent and 1.8 percent respectively have remained steady and early-stage delinquency (1 plus Days Past Due and 30 plus DPD) is also stable.

Source: Company

Source: Company

Credit costs (provision on bad asset as a percentage of loan book) that had spiked to 150 basis points in FY21 has now moderated to 60 basis points and should remain in the sub 1 percent zone barring any major black swan event.

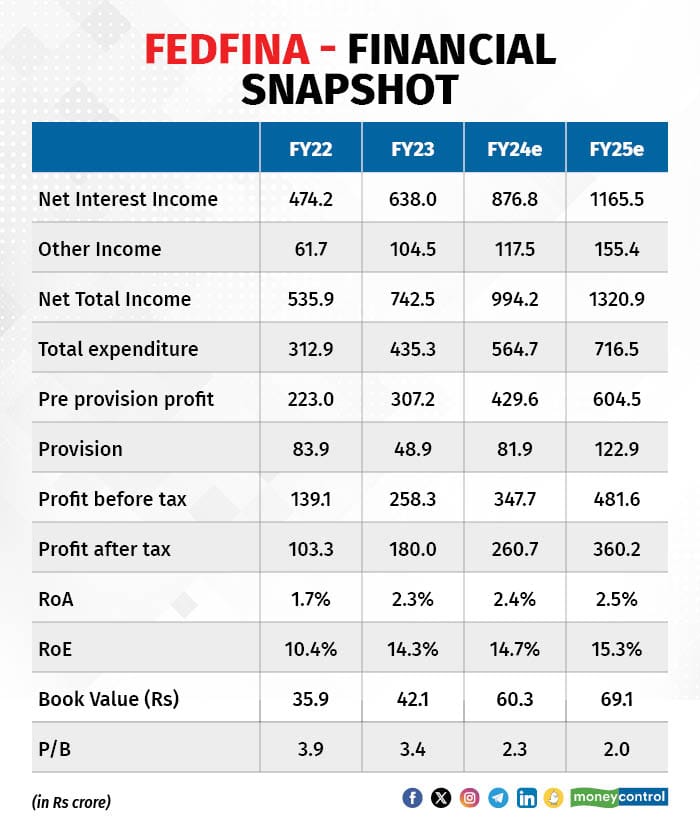

Credit growth is expected to be strong, there is stability in margin and credit cost, and operating expenses are expected to moderated as a large part of the IT implementation is over. Therefore, incremental opex is likely to be linked to business volumes. As a result, the company expects to end the year with an RoA (return asset) of 2.5 percent (2.4 percent in Q2).

Source: Company, Moneycontrol Research

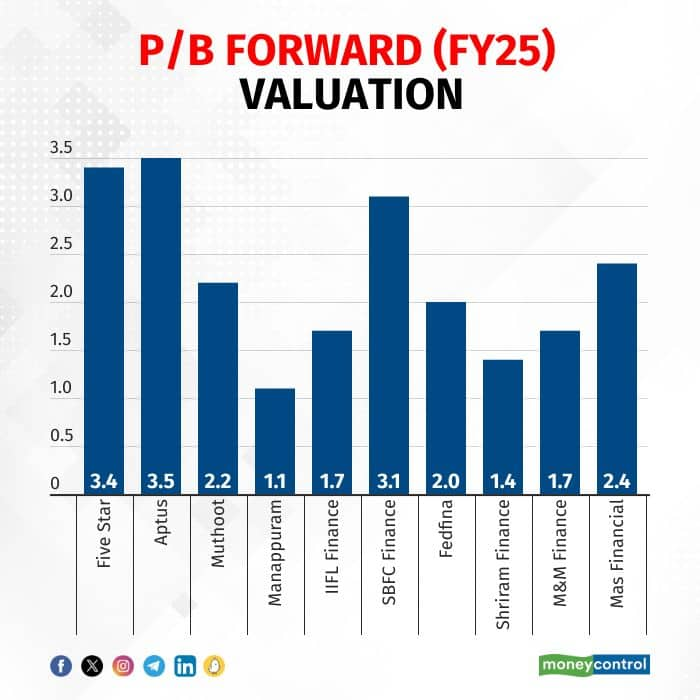

We expect an earnings CAGR in the vicinity of 40 percent in the coming two years and the stock price will gradually take notice of the same. However, we do not expect meaningful multiple rerating.

Source: Moneycontrol Research

Key risks

Growth challenges, steep rise in cost of funding or deterioration in asset quality.

Check Free Credit Score on Moneycontrol: Easily track your loans, get insights, and enjoy a ₹100 cashback on your first check!

Pro Masters Virtual: India on cusp of growth take-off, by Vaibhav Agrawal

Watch more

Pro Masters Virtual: India on cusp of growth take-off, by Vaibhav Agrawal

Watch more  Pro Masters Virtual: Watch ‘Commodity: Gold Investments’ with Somasundaram PR

Watch more

Pro Masters Virtual: Watch ‘Commodity: Gold Investments’ with Somasundaram PR

Watch more  Pro Masters Virtual: Watch “Multicap Funds: A Perfect Balance Between Growth & Stability” with R Srinivasan, Ruchit Mehta, Sukanya Ghosh, Priyanka Dhingra, Saurabh Pant and Nidhi Chawla

Watch more

Pro Masters Virtual: Watch “Multicap Funds: A Perfect Balance Between Growth & Stability” with R Srinivasan, Ruchit Mehta, Sukanya Ghosh, Priyanka Dhingra, Saurabh Pant and Nidhi Chawla

Watch more  Pro Masters Virtual: Watch 'Inter-Market Analysis – How Macro Factors Impact Market Direction?' with Rohit Srivastava

Watch more

Pro Masters Virtual: Watch 'Inter-Market Analysis – How Macro Factors Impact Market Direction?' with Rohit Srivastava

Watch more  Pro Masters Virtual: Watch “Kagi Charts - The Forgotten Technical Analysis Technique” with Brijesh Bhatia

Watch more

Pro Masters Virtual: Watch “Kagi Charts - The Forgotten Technical Analysis Technique” with Brijesh Bhatia

Watch more  Moneycontrol Knowledge Summit: Watch Mayuresh Joshi’s take on “CANSLIM approach for investing and trading”

Watch more

Moneycontrol Knowledge Summit: Watch Mayuresh Joshi’s take on “CANSLIM approach for investing and trading”

Watch more  Pro Masters Virtual: Watch Dr C K Narayan’s take on Profitable Strategies for Active Trading

Watch more

Pro Masters Virtual: Watch Dr C K Narayan’s take on Profitable Strategies for Active Trading

Watch more

Moneycontrol Pro Panorama | Rising passive investment

Dec 27, 2023 / 05:15 PM IST

In this edition of Moneycontrol Pro Panorama: High food inflation can play spoilsport, services pull up current account in latest ...

Read Now

Moneycontrol Pro Weekender: Jerome Powell and the Wizard of Oz

Dec 16, 2023 / 12:47 PM IST

If Powell succeeds in steering the US economy to a soft landing, it will be a remarkable achievement, and history will know him as...

Read Now WATCH: Moneycontrol Pro’s The Consistent Compounders Show—Episode 6

Watch more

WATCH: Moneycontrol Pro’s The Consistent Compounders Show—Episode 6

Watch more  Watch: Moneycontrol Pro’s The Consistent Compounders Show - Episode 5

Watch more

Watch: Moneycontrol Pro’s The Consistent Compounders Show - Episode 5

Watch more  Watch: Moneycontrol Pro’s The Consistent Compounders Show—Episode 4

Watch more

Watch: Moneycontrol Pro’s The Consistent Compounders Show—Episode 4

Watch more  Watch: Moneycontrol Pro’s The Consistent Compounders Show - Episode 3

Watch more

Watch: Moneycontrol Pro’s The Consistent Compounders Show - Episode 3

Watch more  Moneycontrol Pro’s The Consistent Compounders Show—Episode 2 featuring Rajeev Thakkar of PPFAS Mutual Fund

Watch more

Moneycontrol Pro’s The Consistent Compounders Show—Episode 2 featuring Rajeev Thakkar of PPFAS Mutual Fund

Watch more  Watch: Moneycontrol Pro’s The Consistent Compounders Show—Episode 1

Watch more

Watch: Moneycontrol Pro’s The Consistent Compounders Show—Episode 1

Watch more