We are always looking for ways to get around paying taxes. A common technique that many married couples employ for doing so is: the spouse in the higher income-tax bracket buys assets or makes investments in the name of the spouse in the lower tax slab. The intention behind this is to pay lower tax than what would have been applicable on the income from these assets.

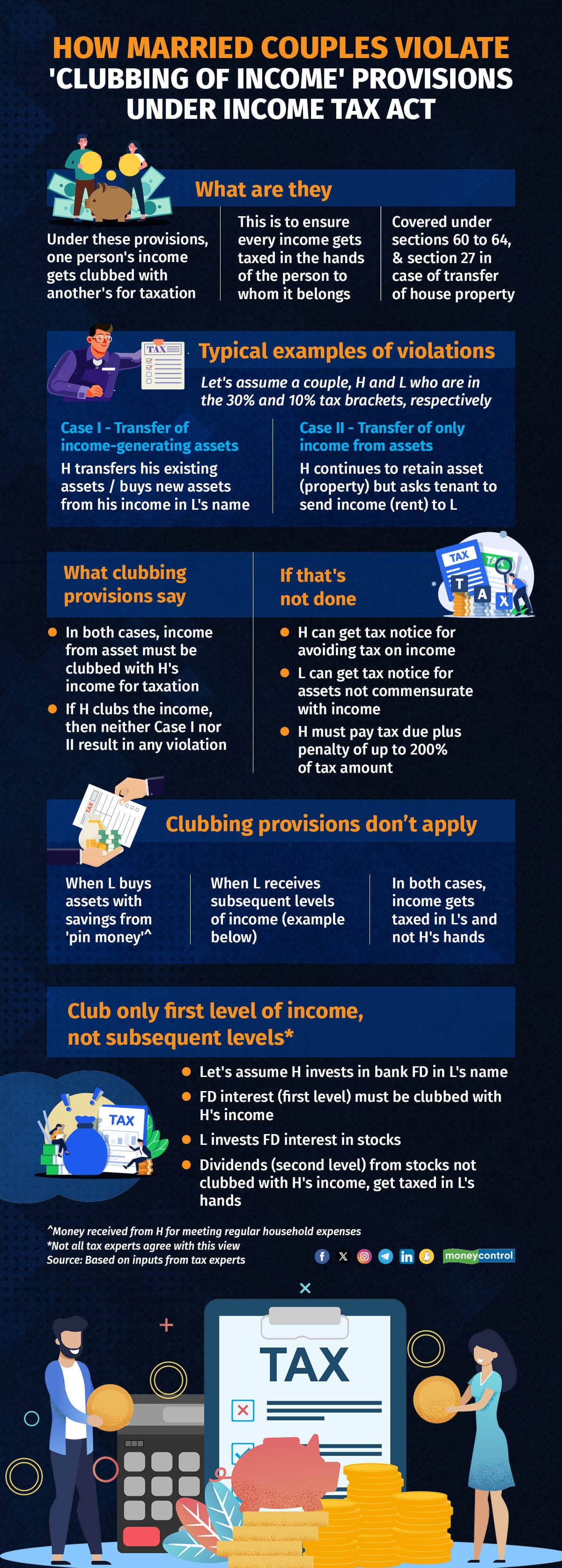

While this may seem like a neat trick, the Income-tax Act has provisions on ‘clubbing of income’ (covered under sections 60 to 64, and also under section 27 in case of transfer of house property) to tackle such situations of tax avoidance.

The modus operandi

How does this typically work? Let’s suppose Mr X is in the 30 percent tax bracket and his wife in the 10 percent one. He uses his income to buy assets (stocks, mutual funds or an immovable property) in his wife’s name or transfers his existing assets to her so that any income from them (dividend from shares, rental income from property or capital gains on sale of shares or property) can be taxed in her hands.

Alternatively, let’s assume he doesn’t transfer say, his property but only the income (rent) from that to her. He asks his tenant to pay the rent into his wife’s account. That way, she can include it in her income which gets taxed at a lower rate.

In both these cases, going by the clubbing provisions, the income from these assets should have been included in the transferor’s (Mr X) income and taxed accordingly. Failure to do so can result in him receiving a notice from the income tax (I-T) department. Then, Mr X will have to pay not only the tax due but additionally, a penalty that can go up to 200 percent of the amount of tax due.

The intention of the clubbing provisions is to ensure that every income is taxed in the hands of the person to whom it belongs. One cannot avoid that by transferring assets (that are income-generating) or the income from those assets to another person.

Also read: Avoid fudged or incomplete documents when submitting tax deduction documents

Jointly-held assets are not a way out

Note that one may not escape the clubbing provisions even if the asset is bought (using one spouse’s income) jointly in the names of both the spouses. In fact, this may bring in some practical complexities, especially if you are trying to be on the right side of the law.

According to Chetan Chandak, director of TaxBirbal, a tax firm, the law is very clear that how the investment is made (who is the primary holder and who is the secondary holder) will not govern taxation. “The income from such an asset should be clubbed with the income of the spouse (whether primary or secondary holder) who made the contribution and taxed as such. The TDS (tax deducted at source) will get deducted in the PAN of the primary holder but TDS does not govern taxability. If the contributing spouse is the secondary holder, he or she can claim the TDS (under the TDS schedule) that was deducted against the other spouse’s PAN when filing tax returns,” Chandak explained.

What happens if both the spouses have contributed to the asset? “Any income from such an asset should be accounted for by both spouses in their respective ITRs (income tax returns) in proportion to their respective contributions,” said Mayank Mohanka, founder, TaxAaram.com, and managing partner, S M Mohanka & Associates. To comply with the clubbing provisions, he suggests that both spouses furnish a declaration to the bank to deduct TDS in proportion to their respective contributions under their respective PANs. Alternatively, the TDS credit reflected in one spouse’s (usually the primary account holder) PAN can be apportioned to the other spouse at tax-filing time (as mentioned earlier). Mohanka says the latter practice is more prevalent.

But as Karan Batra, founder of CharteredClub.com, a tax firm, points out, sometimes what is legally right and what is practically possible can be very different. He said, “Couples contribute and invest together and it may sometimes happen that the main contributing spouse is the secondary holder in an asset. They may not have done this deliberately to reduce their tax outgo (say, both are in the same tax bracket) but they will still have to be careful about who pays the tax.”

Mohanka said that sometimes where the TDS has been deducted in one spouse’s name (reflected in Form 26AS) but the other spouse correctly clubs the income and pays the tax, the first spouse may still receive a tax notice. Then, taking the example of shares, Mohanka highlighted an instance of how things can go wrong. “Say one spouse (higher tax bracket) transfers his or her shares to the other spouse, who then sells these shares after many years have passed. Legally the first—and not the second—spouse should pay the capital gains tax. But if that happens, then the second spouse who owns the shares may receive a tax notice.”

On the other hand, another tax expert, who did not wish to be named, mentioned that sometimes couples get away with investing their income in each other’s names. This person spoke about how many couples jointly hold real estate properties where the contribution has come from only one spouse. When it comes to paying tax on rent or capital gains tax on sale of the property, they split it evenly and get away with it as the asset ownership is joint. However, once the amounts involved go up, and if one spouse consistently has no or low income, getting a tax notice becomes a real possibility.

When clubbing provisions may not apply

There are, however, a few situations where the clubbing provisions do not apply.

One, in case of pin money—money given by one spouse to another for meeting regular household expenses. “If a spouse is able to save some part of the pin money for investing, then the clubbing provisions do not apply to the income from such assets,” said Chandak.

Then, what about the possibility of a spouse misusing this by transferring a large part of his or her income to the spouse as pin money? To that, Chandak said, “While pin money can be subjective as it has not been defined anywhere, there has to be some reasonability to it.” In short, if someone transfers the bulk of his or her income to the spouse as pin money, it will catch the tax department’s attention.

Two, according to a few tax experts, the clubbing provisions apply only to the first level of income. This can help with tax planning. So, if we go by the earlier example, any rental income (first level of income) from the property in Mr X’s wife’s name will be taxed in Mr X’s hands. But if his wife invests this rental income in, say, a fixed deposit, then the interest income (second level of income) will be taxed as part of her income. Clubbing provisions will not apply to it.

According to Chandak, the clubbing provisions under the I-Tax Act cover only the income generated from the transferred asset (that is, first level of income) and are silent on the income generated from the income from this asset (subsequent levels of income). Batra too, agreed that clubbing applies only to the first level of income and not subsequent incomes. But others such as Mohanka say that strictly speaking, clubbing should apply even to subsequent incomes but this is a grey area.

Offering a long-term solution to the income clubbing violations, Mohanka suggested that India adopt the system of filing of a joint tax return by a couple as in other jurisdictions such as the US and UK.

Check Free Credit Score on Moneycontrol: Easily track your loans, get insights, and enjoy a ₹100 cashback on your first check!